Medicare Basics: What is Medicare & How Do I Apply?

Medicare Basics

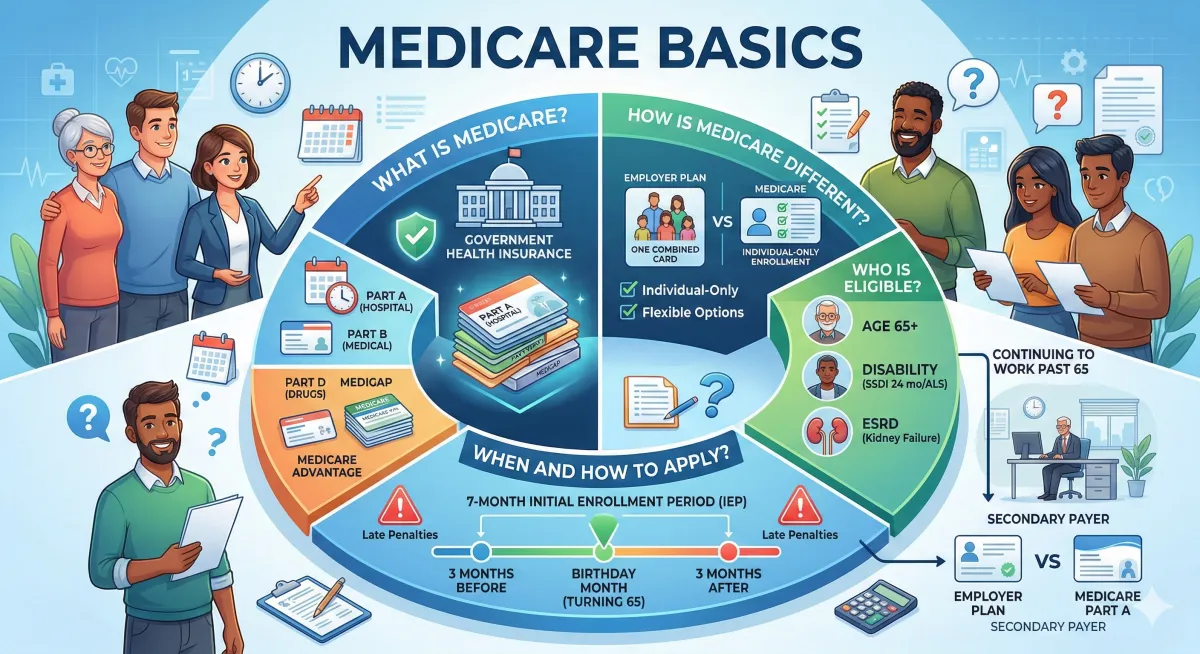

What is Medicare?

Medicare is a government health insurance program that provides certain coverage and benefits. Unlike previous health insurances, Medicare comes with diverse plan choices. It also has important sign-up deadlines and rules to adhere to. Let us guide you through understanding these details.

How is Medicare Different From Other Health Insurance?

Medicare differs from employer health insurance in some key ways. Employer plans often bundle medical and prescription drug benefits and can cover you and your spouse. In contrast, Medicare is individual-only; each person needs their own enrollment. Plus, it offers flexible options for how you receive your benefits.

Medicare covers individuals, not couples, so you and your spouse need to sign up independently. It offers flexibility in how you get your benefits, allowing you to:

Select the standard hospital and medical plan managed by the federal government.

Opt for additional prescription drug coverage through a private provider.

Buy extra insurance to help pay for what Medicare doesn't.

Choose an all-in-one private insurance plan that includes hospital, medical, and often drug coverage.

Medicare lets you tailor your healthcare coverage to suit your personal preferences and financial situation. We're here to help you make the most of these choices.

Who is Eligible for Medicare?

You are generally eligible for Medicare if you meet one of the following criteria:

Age 65 or older: If you are a U.S. citizen or legal resident who has lived in the U.S. for at least 5 years, you are eligible for Medicare at age 65.

Younger than 65 with a disability: You may be eligible if you have received Social Security Disability Insurance (SSDI) for 24 months or have Amyotrophic Lateral Sclerosis (ALS).

End-Stage Renal Disease (ESRD): If you have permanent kidney failure requiring dialysis or a transplant, you are eligible for Medicare.

When and How to Apply for Medicare?

Most people enroll in Medicare when they're about to turn 65. You have a 7-month Initial Enrollment Period that starts three months before your 65th birthday, includes your birthday month, and extends three months after your birthday. Missing this enrollment window means risking late fees for Part B and Part D, plus losing key health and financial protections. You'll want to enroll in Medicare as soon as you're eligible. How you enroll in Medicare depends on whether you’re already receiving Social Security, Railroad Retirement Board, or Office of Personnel Management benefits.

If you ARE currently receiving benefits from Social Security, Railroad Retirement Board, or Office of Personnel Management at least 4-months before you turn 65:

You’ll automatically get Medicare Part A and Part B starting the first day of the month you turn 65.

If your birthday is on the first day of the month, Part A and Part B will start the first day of the prior month.

If you ARE NOT receiving benefits from Social Security, Railroad Retirement Board, or Office of Personnel Management benefits at least 4-months before you turn 65:

You’ll need to sign up with Social Security to get Medicare Part A and Part B.

You can apply online at socialsecurity.gov, at your local Social Security office or by calling Social Security at 1-800-772-1213 (TTY: 1-800-325-0778).

If you worked for a railroad, call the RRB at 1-877-772-5772.

If you have ESRD (End Stage Renal Disease), you can choose to enroll in Part A and Part B:

You’ll need both Part A and Part B to qualify for the full benefits that cover certain dialysis and kidney transplant services.

You can apply online at socialsecurity.gov, at your local Social Security office or by calling Social Security at 1-800-772-1213 (TTY: 1-800-325-0778).

Continuing to Work Past the Age of 65

Turning 65 doesn’t always mean you have to sign up for Medicare right away — especially if you’re still working. If you or your spouse are actively employed by a company with 20 or more employees and you’re receiving health insurance through that employer, you can:

Stay with the employer health plan as your primary coverage and delay Medicare enrollment.

Enroll in Medicare Part A and use it as secondary coverage to help pay for things the employer health plan doesn’t cover.

Choose to delay enrolling in Medicare Part B until the employment ends or the coverage stops, without paying late enrollment penalties if you enroll later.

Frequently Asked Questions

1. How does Medicare differ from the health insurance I have through my employer?

Unlike employer plans that often cover families or spouses, Medicare is strictly individual. Each person must enroll independently. Additionally, while employer plans typically bundle all benefits together, Medicare offers the flexibility to choose between government-managed plans (Part A and B) or private options like Medicare Advantage and Supplemental insurance.

2. When is the best time to sign up for Medicare?

For most people, the best time is during your Initial Enrollment Period (IEP). This is a 7-month window that begins three months before the month you turn 65, includes your birth month, and ends three months after. Enrolling during this time helps you avoid late enrollment penalties and gaps in coverage.

3. Do I need to enroll in Medicare if I am still working past age 65?

If you or your spouse are still working and covered by an employer health plan (at a company with 20 or more employees), you may be able to delay Medicare Part B without penalty. However, many people still choose to enroll in Part A at 65 because it is usually premium-free and can act as secondary insurance.

4. Will I be enrolled in Medicare automatically?

Enrollment is only automatic if you are already receiving benefits from Social Security or the Railroad Retirement Board at least four months before you turn 65. If you are not yet receiving these benefits, you must manually sign up through the Social Security Administration online or at a local office.