The $2,300 Toenail: Medicare HMO Out-of-Network Rules

The $2,300 Toenail: The Hidden Risks of HMO Plans

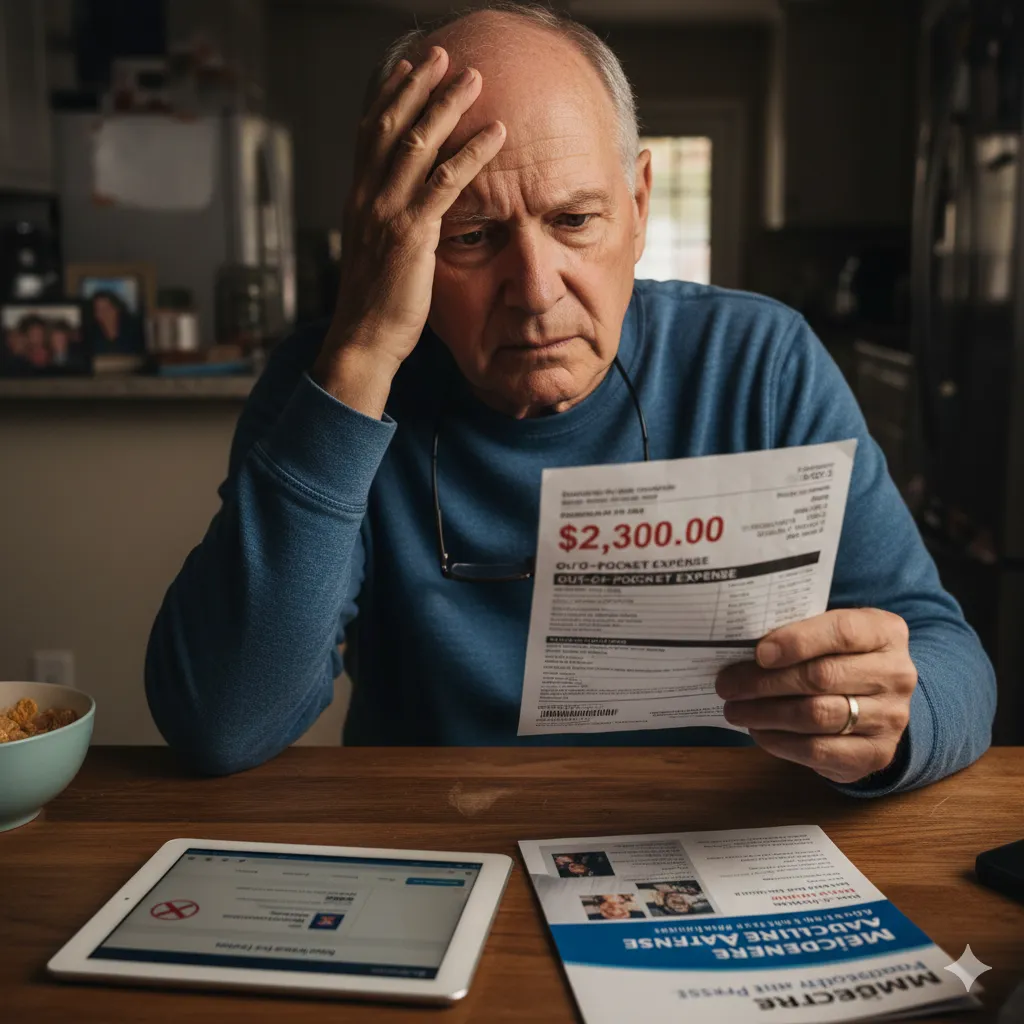

I received a call from a client recently that perfectly illustrates why understanding your Medicare Advantage plan is so critical. She was shocked and looking for answers; she had just received a $2,300 bill after her husband had a procedure for a recurring ingrown toenail.

After some research, we discovered the root of the problem. While her husband thought he was going in for a simple fix, the clinic performed a Matrixectomy, which is a surgical procedure to permanently remove the nail root.

Because it was a formal surgery, the costs were high. However, the real sting came from the insurance: her husband had made the appointment without checking to see if the podiatrist was in their plan’s HMO (Health Maintenance Organization) network. He was not. Because the doctor was out-of-network, the plan refused to pay a single cent, which left them responsible for the full surgical bill.

The Rules of the Road

Unlike a PPO (Preferred Provider Organization) or even an HMO-POS (Point-of-Service option), a standard HMO has strict rules concerning out-of-network providers. Generally, it only covers services performed by network providers, with the exception of medical emergencies.

This got me thinking: how many Medicare beneficiaries enroll in a plan and, over time, forget the specific "rules of the road"? To help you avoid large healthcare expenses that do not count toward your annual out-of-pocket maximum, let’s break down the basics of how HMO networks work.

Why Networks Matter (and Why it Costs So Much)

Here is the uncomfortable truth about out-of-network bills: they are the stealth bombers of healthcare. Even in 2026, they can blindside you when you least expect it; they leave your financial safety net untouched and your bank account vulnerable.

In an HMO network, the insurance company contracts with specific groups of doctors and hospitals. In exchange for a steady stream of patients, these providers agree to lower their rates. However, this is a two-way street. If you step outside that circle for routine care, the contract is effectively broken; consequently, the insurance company is no longer obligated to pay its share.

The "MOOP" Trap

The most painful consequence of an out-of-network bill is that it does not count toward your Maximum Out-of-Pocket (MOOP) limit. The federal government sets a MOOP limit as a safety net for Medicare beneficiaries. For 2026, the statutory ceiling is $9,250, though many individual plans set their limits much lower. This figure represents the absolute maximum you should have to pay for covered, in-network care in a single year.

Because my client’s husband bypassed network requirements, his $2,300 procedure did not contribute a single cent toward his MOOP limit. The safety net stayed untouched while he footed the entire bill alone. This is the "hidden" reality of many HMOs: without a referral or an in-network provider, the financial protections you think you have simply vanish.

The Three Exceptions: When the HMO Must Pay

Even with strict rules, there are three times your HMO is legally required to cover you, even if the doctor is out-of-network:

True Emergencies: If you have a life-threatening situation, go to the nearest ER. You will only be charged your standard in-network copay.

Urgent Care (Out of Area): If you are traveling and need immediate care for something like a high fever or a minor injury, you are covered.

No In-Network Specialist Available: If the HMO does not have a qualified doctor in their network for a specific treatment, they must allow you to see an outsider. But beware: you must get "prior authorization" in writing before the appointment.

Comparing Plan Flexibility

To help you visualize the differences, here is how the most common plan types handle out-of-network care:

How to Protect Yourself

To ensure you are not surprised by a massive bill, follow these three steps every time you book an appointment:

Ask the Right Question: Instead of asking "Do you take Medicare?", ask: "Are you in-network for my specific [Plan Name] HMO?"

Check the Portal: Log in to your insurance company’s website and use their "Find a Provider" tool. It is the most up-to-date resource available.

Referrals are Key: In most HMOs, you need a referral from your Primary Care Physician (PCP) to see a specialist. If you skip this step, the bill might stay with you.

Do not let a simple procedure turn into a financial headache. A five-minute phone call to verify a doctor's network status can save you thousands.

Are you unsure which type of plan you currently have? I can help you look up your plan's summary of benefits so you know exactly where you stand before your next appointment. Would you like me to do that for you?